New Tax Legislation 2026: What Will Change for Sole Proprietors and LLCs

Key Tax Indicators for Business in 2026

Taxes for individual entrepreneurs (FOP) and LLCs in 2026 depend on two basic social indicators: the minimum wage and the subsistence minimum for able-bodied persons. From January 1, 2026, the minimum wage is 8,647 UAH, and the subsistence minimum for able-bodied persons is 3,328 UAH. Fixed payments, income limits, SSC, and military tax are calculated based on these amounts.

For entrepreneurs and companies, it is important not only to know the rates but also to check how they affect monthly tax payments, reporting, cash discipline, contracts, pricing, and the choice of taxation system.

- FOP taxes in 2026 depend on the single tax group, annual income, presence of employees, and VAT payer status;

- taxes for LLCs depend on the taxation system, profitability, VAT presence, number of employees, and type of activity;

- the single tax for FOP groups 1 and 2 in 2026 is tied to the subsistence minimum or minimum wage;

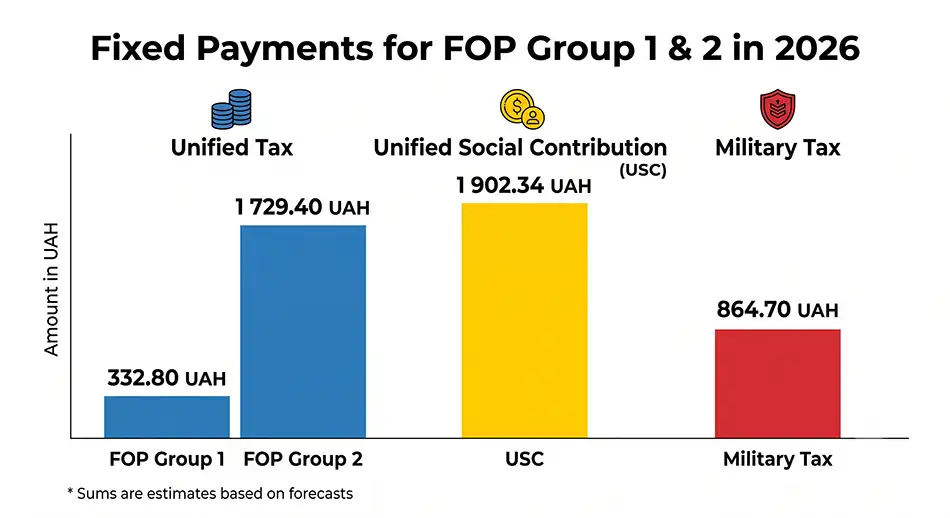

- the minimum SSC for FOP in 2026 is 1,902.34 UAH per month, i.e., 22% of the minimum wage;

- the military tax for FOP groups 1 and 2 in 2026 is 864.70 UAH per month, and for group 3 – 1% of income;

An entrepreneur should calculate not only the tax burden but also the minimum profitability of each business area. For LLCs, it is critical to review the financial model since profit tax, VAT, payroll taxes, and dividends together form the total cost of legally withdrawing funds.

You can order a consultation with qualified accountants here. Receive maintenance offers and choose the best terms.

FOP Group 1 in 2026

Group 1 FOP taxes in 2026 remain fixed, but amounts have increased due to new social indicators. According to the SFS, the annual income limit for FOP Group 1 is 1,444,049 UAH, the single tax is up to 332.80 UAH per month, the minimum SSC is 1,902.34 UAH per month, and the military tax is 864.70 UAH per month.

This group is suitable for the smallest microbusiness without hired employees but requires control over annual turnover and allowed types of activities.

- Check the local single tax rate, as the maximum amount of 332.80 UAH may be lower depending on community decisions.

- Control income within 1,444,049 UAH per calendar year.

- Include SSC, military tax, and single tax in the monthly budget.

- Do not use Group 1 for activities that do not meet the simplified system conditions.

- Verify payment details before each tax payment.

For the query “Group 1 FOP taxes,” the main change in 2026 is not a new rate per se, but the increase in monetary amounts due to the minimum wage and subsistence minimum. Tax payments must be included in the payment calendar to avoid debt and the risk of losing the simplified system.

FOP Group 2 in 2026

Group 2 FOP taxes in 2026 suit small businesses, trade, services to the population, and single tax payers. The income limit for FOP Group 2 is 7,211,598 UAH, the single tax is up to 1,729.40 UAH per month, the minimum SSC is 1,902.34 UAH per month, and the military tax is 864.70 UAH per month.

For entrepreneurs in this group, the tax burden is predictable, but fixed payments must be made even in months with low income unless there are legal grounds for exemption.

- fixed single tax does not depend on actual monthly turnover;

- military tax is paid monthly in a fixed amount;

- SSC for oneself minimally is 1,902.34 UAH per month;

- the annual limit of 7,211,598 UAH must be controlled through bank receipts and cash transactions;

- when approaching the limit, it is advisable to evaluate in advance the transition to FOP Group 3 or LLC;

For the query “Group 2 FOP taxes,” the practical action is to make a financial plan for the year. If the business is seasonal, fixed payments should be allocated so that tax liabilities do not create cash gaps during low sales periods.

FOP Group 3 in 2026

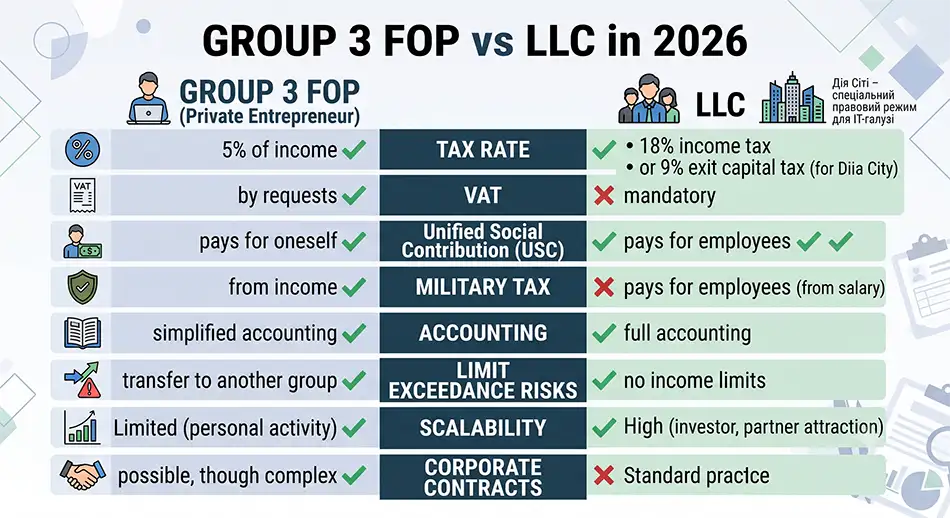

The taxes for FOP group 3 remain the most flexible for services, online business, IT, consulting, marketing, e-commerce, and work with legal entities. In 2026, for FOP group 3 the annual income limit is 10,091,049 UAH, the single tax rate is 5% of income without VAT or 3% of income with VAT, the minimum USV is 1,902.34 UAH per month, and the military levy is 1% of income.

FOP group 3 is beneficial when expenses are not a significant part of turnover or when simplicity of accounting is more important than the ability to reduce the taxable base by expenses.

- Calculate the actual burden: 5% single tax plus 1% military levy from income.

- Compare the 5% without VAT and 3% with VAT models if contractors require a tax credit.

- Maintain records of receipts for all accounts, cash, acquiring, and marketplaces.

- Monitor the limit of 10,091,049 UAH until the end of the year.

- Check whether the activity is not among those prohibited for the simplified system.

A separate change in 2026 concerns security activities: Law №4698-IX has excluded it from the simplified system starting January 1, 2026, so both FOP and legal entities engaged in such activity need to switch to the general system or change their business structure.

Taxes for LLC in 2026

Taxes for LLC in 2026 depend on whether the company operates under the general system or the single tax. For LLCs on the general system, the basic corporate income tax rate is 18%, while banks have a separate rate of 50% in 2026 according to specific changes in Law №4698-IX.

LLCs have broader opportunities for scaling, working with large contractors, participating in tenders, and attracting investors but accounting is more complex than for FOP.

- Corporate income tax for LLC – 18% of financial result considering tax differences;

- VAT – 20% if the LLC is registered as a VAT payer or obliged to register;

- USV for employees – 22% on the payroll fund;

- Personal income tax (PIT) on employees’ salaries – 18%;

- Military levy on salary – 5%;

- Dividends to founders are taxed separately depending on the taxation system and the recipient’s status;

An LLC under the single tax of group 3 can apply a rate of 5% without VAT or 3% with VAT if it meets the conditions of the simplified system. This model is often used by small and medium businesses that need a legal entity but do not require the full corporate income tax model.

VAT, Reporting and Tax Payments in 2026

Mandatory VAT registration under the general rule occurs if the volume of taxable operations for the last 12 calendar months exceeds 1,000,000 UAH without VAT, but this rule has exceptions for single tax payers of groups 1-3. The State Tax Service in 2026 confirms this registration criterion.

Reporting has also changed: for FOP and self-employed persons regarding PIT, military levy, and USV starting from 2026, a quarterly format of submission applies, while legal entities continue to report monthly. The State Tax Service indicated that the deadline for FOP is 40 calendar days after the quarter ends.

- Create a calendar for paying single tax, USV, military levy, VAT, and corporate income tax.

- Check the 2026 annual FOP limits before signing large contracts.

- Update contracts, acts, invoices, payment purposes, and NACE codes.

- Verify that the business does not trigger an obligation to register as a VAT payer.

- Separate personal and business payments to avoid accounting errors.

- Review prices taking into account the increase of USV, military levy, and payroll taxes.

The new tax legislation for 2026 is not just about new amounts. For sole proprietors, the main thing is to control income limits, group classification, VAT, and prohibited types of activities; for limited liability companies, it is important to properly plan corporate income tax, VAT, payroll taxes, dividends, and documentation workflow.