How the Polish Tax System Works Business taxation in Poland depends on the legal-organizational form, residency, type of activity, turnover, and profit distribution method. A limited liability ...

17Jul

Taxes for business in Cyprus are formed according to the model of European jurisdiction with corporate taxation, VAT, rules of tax residency, audit, electronic reporting, and economic presence requirements. Cyprus should not be considered a classic offshore company jurisdiction, as the country operates within EU legislation, applying transparency rules, controlled foreign companies regulations, transfer pricing, and international tax information exchange.

The basis of the tax burden for a Cyprus company consists of several mandatory payments. They depend on the type of activity, income source, ownership structure, presence of employees, real estate transactions, operations with the EU, and tax residency status.

The Cypriot tax system is not limited merely to a low corporate tax rate. For business, rules on expense recognition, income source, substance, audit, contract accuracy, documentation of related-party transactions, and timely reporting submission are important.

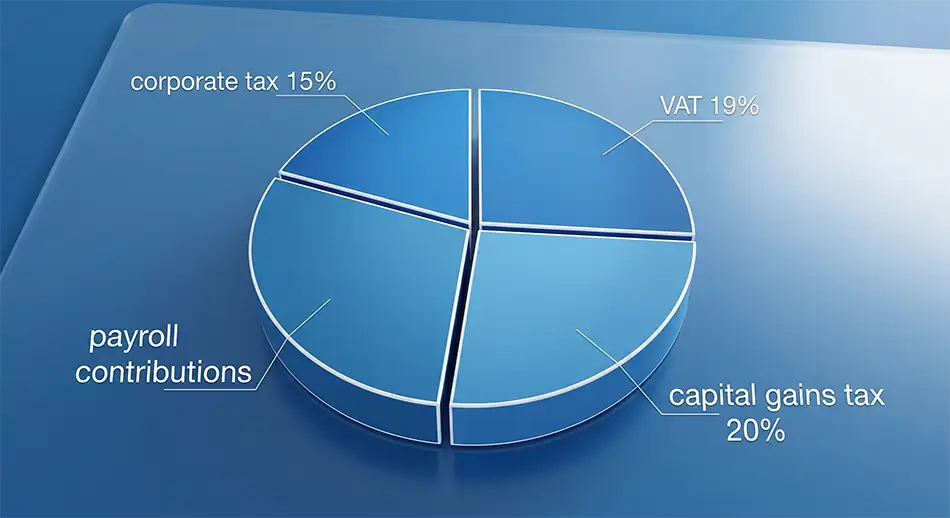

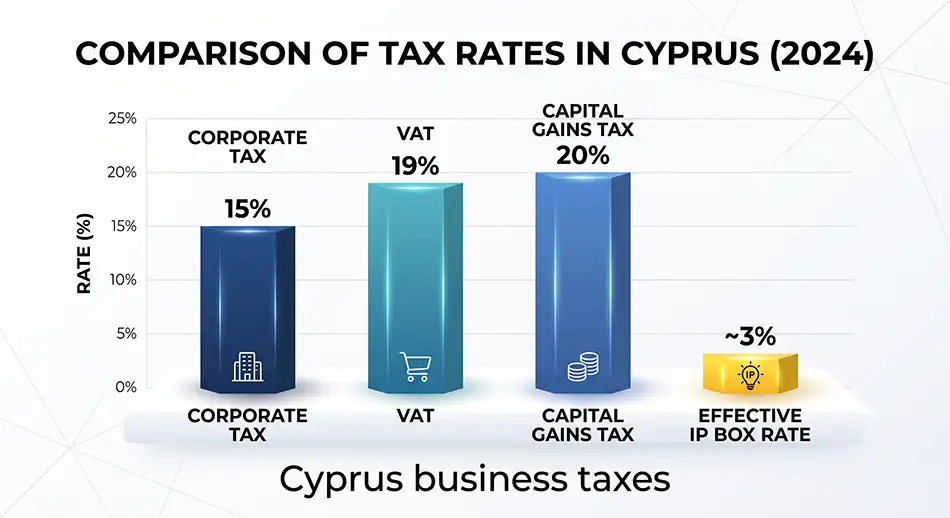

From January 1, 2026, the standard corporate tax rate in Cyprus is 15%. Tax is paid not on turnover but on taxable profit, i.e., income after deducting allowable expenses, adjustments, and benefits.

For business, this means that the actual tax burden depends not only on the rate but also on the quality of financial accounting. The company must confirm expenses with documents, contracts, invoices, acts, bank payments, and the economic logic of operations.

Corporate tax is the central element of the system, but it does not operate in isolation. For international business, double taxation treaties, dividend payment rules, transfer pricing, VAT, and beneficiary tax status are simultaneously significant.

A Cypriot company may be taxed as a tax resident of Cyprus if its management and control are exercised from Cyprus or if the rules provided by current tax legislation apply. For international structures, this issue is practically significant since formal registration without real management may create risks in another country.

Tax residency is confirmed not by a single document but by a combination of factors. The tax office and banks pay attention to where management decisions are actually made, who signs key documents, where corporate documentation is kept, and how the company conducts operational activities.

Residency is especially important for holding companies, IT businesses, trading structures, consulting, financial operations, intellectual property licensing, and working with partners from the EU. If management actually takes place from another country, a conflict of residency or taxation under foreign jurisdiction rules may arise.

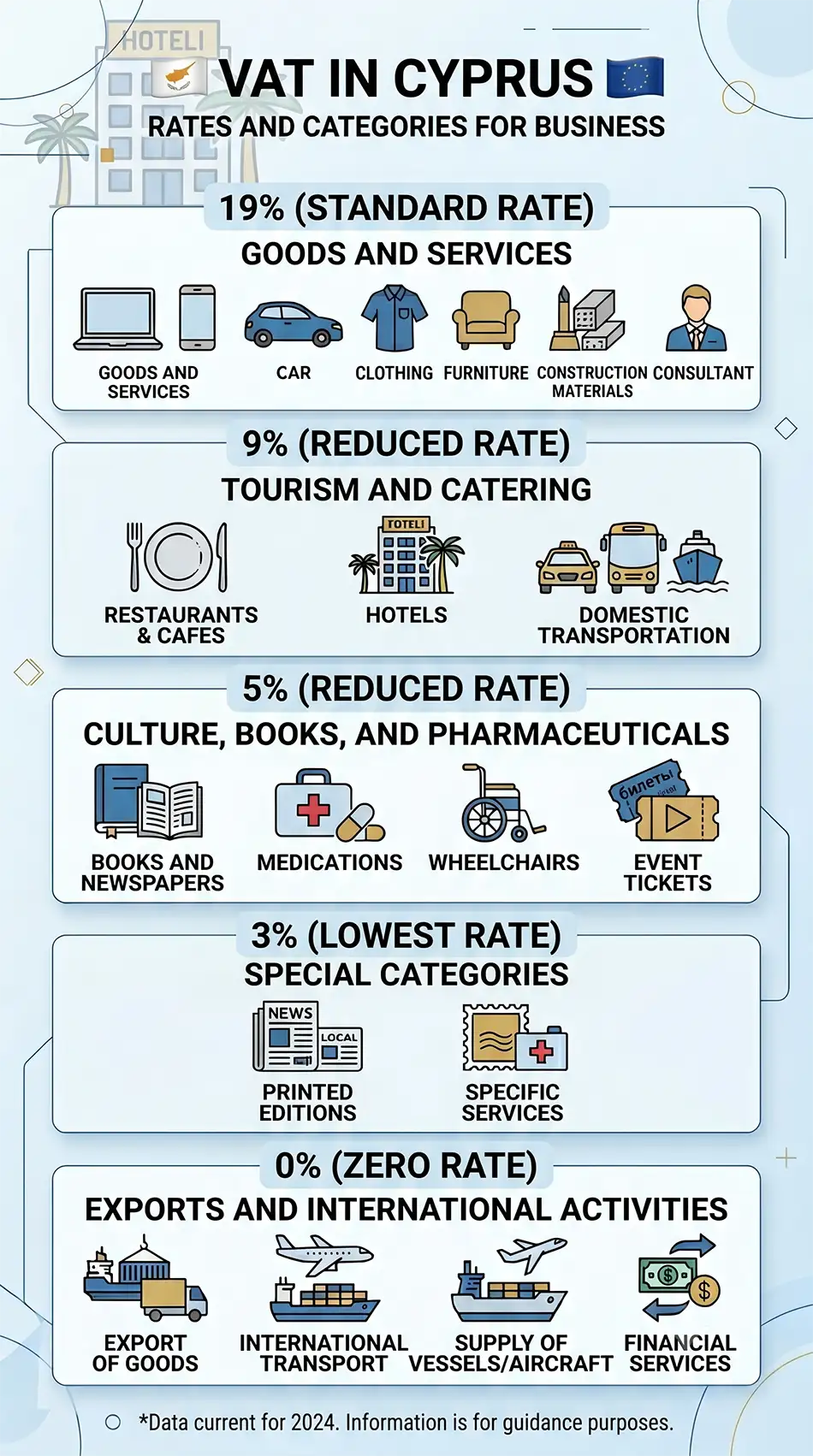

VAT in Cyprus applies to the supply of goods and services, import of goods, acquisition of goods from other EU countries, and certain cross-border operations. The standard rate is 19%, but reduced rates apply to some goods and services.

Mandatory VAT registration occurs if the taxable turnover over the previous 12 months exceeds €15,600 or is expected to exceed this threshold within the next 30 days. Separate rules also apply for acquisitions of goods from other EU countries, intra-European supplies, and reverse charge.

VAT is not only a tax but also a part of documentation flow. A company must correctly determine the place of supply, status of the counterparty, presence of reverse charge, right to tax credit, and the period when the operation is recognized.

One reason Cyprus is used for international structures is its rules for paying dividends, interest, and royalties to non-residents. In many typical cases, Cyprus does not withhold tax when paying dividends and interest to non-residents, but since 2026, special rules must be considered for related companies in low-tax or undesirable jurisdictions.

For business owners, it is important to distinguish three levels of taxation. The first is the tax of the Cyprus company on its profit. The second is potential withholding tax upon income distribution from Cyprus. The third is the taxation of the dividend recipient in their country of tax residence.

Te dividend model requires analysis not only of Cyprus law but also the rules of the owner’s country. For Ukrainian, European, or other foreign beneficiaries, rules of CFC (Controlled Foreign Company), foreign income declaration, currency control, and requirements to confirm the source of funds may apply.

In Cyprus, capital gains tax mostly relates to real estate. The 20% rate applies to profits from selling immovable property located in Cyprus, as well as to certain transactions involving shares or stakes in companies whose value directly or indirectly comes from Cypriot real estate.

For trading, IT, consulting, or holding companies, this tax is often not key. It becomes important if the structure owns land plots, commercial real estate, residential buildings, or stakes in companies owning property assets in Cyprus.

Before a real estate transaction, it is necessary to calculate not only the capital gains tax but also VAT, stamp duty, registration fees, legal formalities, and the impact of the deal on the company’s financial statements.

IP Box is one of the important tax regimes in Cyprus for companies generating income from qualifying intellectual property. The regime can allow an 80% deduction of qualifying profits from relevant IP assets, including software, patents, and certain technological solutions.

For IT businesses, this regime matters when the company not only receives payment for services but owns or economically controls the intellectual asset. Not every website, brand, domain, marketing name, or commercial designation qualifies for the IP Box.

IP Box does not function as an automatic discount for any technology company. There must be a link between income and the qualifying asset, the proper legal structure, accounting for development expenses, agreements with developers, and confirmation of economic substance.

Notional Interest Deduction is a mechanism for a notional interest deduction for companies financed by new equity capital. Its logic is that equity receives a tax deduction similar to interest on debt financing but without actual interest payments.

This tool can be useful for structures with real capital, investment activities, financing of subsidiaries, or active operational business. At the same time, the deduction should not be artificial and requires documentary justification.

Notional Interest Deduction should not create a tax arrangement lacking commercial substance. Its application requires financial modeling, confirmation of capital sources, corporate resolutions, and accurate audit presentation.

The Cyprus system allows for the accounting of tax losses in future periods according to established terms and rules. After the 2026 tax reform, the loss carryforward period was extended to 7 years, which is significant for startups, investment projects, and businesses with uneven profitability.

Group planning enables structuring activities so that profitable and loss-making companies within the group operate coherently. However, such mechanisms require compliance with ownership, residency, and documentary conditions.

For businesses with significant startup costs, this creates room for tax planning. At the same time, losses should not be artificial, and the structure should not exist solely to shift the tax base.

Transfer pricing applies to transactions between related parties. If a Cypriot company provides services to a parent company, receives royalties, finances subsidiaries, buys goods from affiliated suppliers, or sells products to a related distributor, the prices must comply with the “arm’s length” principle.

Tax authorities assess whether independent companies would behave similarly under comparable conditions. If the price, margin, or contract terms do not correspond to market levels, a profit adjustment may arise.

Transfer pricing is especially important for IT outsourcing, marketing services, management fees, royalties, intra-group financing, and international trade. A formal contract without actual work execution does not protect the company from tax issues.

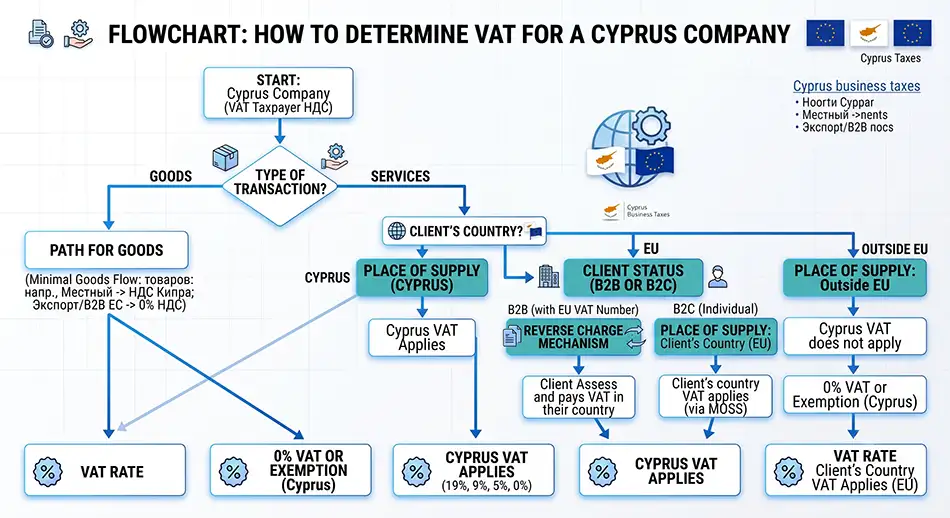

A Cypriot company working with EU clients must correctly determine the VAT regime for each transaction. For B2B services, the place of supply rule usually applies according to the recipient’s country, but exceptions may concern real estate, events, electronic services, transport, import, and local operations.

The most common mistake is assuming that an international contract automatically has no VAT. In fact, one must verify the client’s status, their VAT number, place of supply, nature of the service, and the presence of reverse charge.

For ecommerce, SaaS, online platforms, and digital services, additional consideration must be given to OSS rules, sales to individuals in the EU, and thresholds for cross-border operations. Such models should be set up before starting sales, not after accumulating turnover.

If the company employs workers in Cyprus, employer obligations arise. This includes registration as an employer, payroll accounting, withholding taxes and contributions, submitting payroll reports, and compliance with labor legislation.

For international owners, it is important not to confuse the status of director, consultant, freelancer, and employee. An incorrect model can create tax risks, claims from social authorities, and questions regarding substance.

The presence of personnel can strengthen the company’s economic presence in Cyprus. At the same time, it increases administrative burden, requiring regular accounting and document preparation.

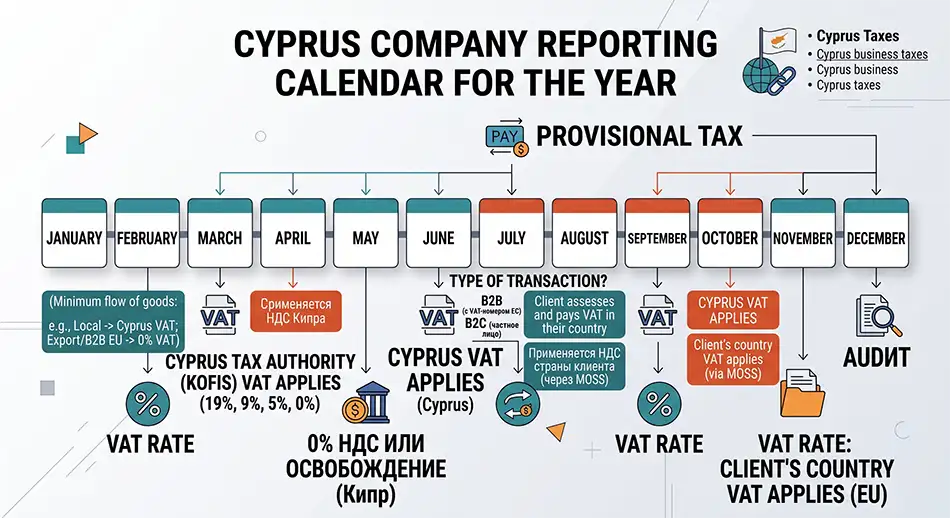

Cyprus companies must keep accounting records, prepare financial statements, undergo audits, and submit tax returns. The reporting year usually corresponds to the calendar year, and tax returns are submitted electronically.

For a company owner, it is practically important to understand that the annual reporting in Cyprus is not just a single form. It consists of accounting data, audit, tax return, corporate annual return, and, if necessary, VAT, VIES, payroll, and transfer pricing documentation.

Quality accounting service is necessary not only for the tax return but also for the bank, audit, confirmation of the origin of funds, dealing with counterparties, and preparation for possible inspections.

Book an accountant consultation here.

Companies in Cyprus pay provisional income tax during the year. It is usually based on the projected profit of the current year and is paid in two installments.

The provisional payment system requires cash flow planning. If the company underestimates profit, additional payments, interest, or penalties may arise. If the forecast is overestimated, the business effectively freezes part of the funds until the final calculation.

For businesses with seasonality, uneven contracts, or large one-time deals, it is important to regularly update the profit forecast. This reduces the risk of overpayment or underpayment of tax.

Every Cyprus company must submit an annual return to the Registrar of Companies. For a new company, the date of the first annual return is related to the completion of 18 months from incorporation, and thereafter reports are submitted annually.

The annual return reflects corporate information about the company. It does not replace the tax return but is an important part of corporate compliance.

Failure to comply with corporate reporting can lead to fines, problems with the bank, difficulties when changing directors or shareholders, risk of company deregistration, and blocking of future corporate actions.

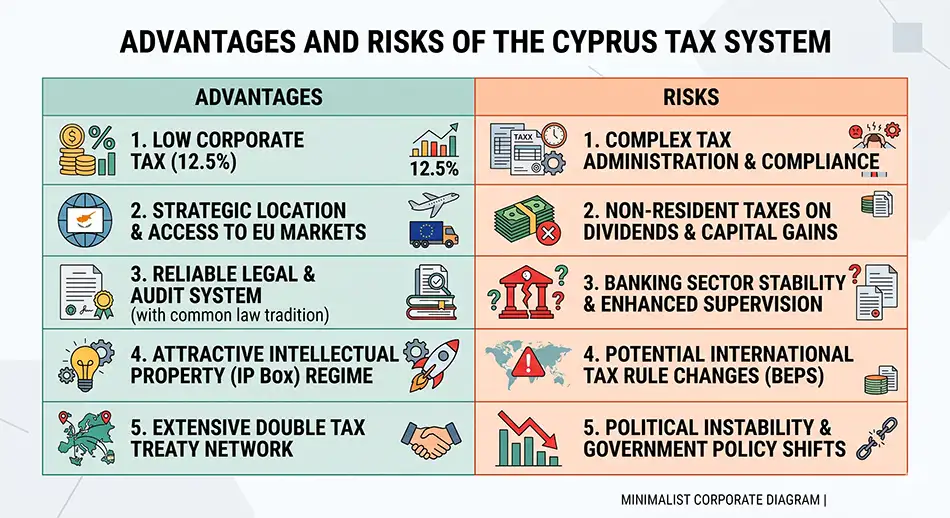

The Cyprus tax system has a number of practical benefits for international business. These manifest not only in rates but also in the predictability of rules, access to the European market, legal system, and the ability to structure business within the EU.

These advantages are most significant for companies that work with international clients, hold intellectual property, earn profits outside the owner’s country, or plan to develop a European presence.

Advantages work only when the structure corresponds to the real business model. A company without management, documentation, accounting, and economic presence can lose tax efficiency.

Cyprus is not a universal solution for any business. After strengthening international transparency rules, formal structures without real activity have become less practical and more risky.

The main disadvantages are not related to rates, but to costs of support, audit, compliance, banking checks, CFC rules in the owner’s country, and the need to maintain real substance in the company.

Before launching a structure, it is necessary to calculate not only the tax but also the total cost of maintaining the company. For small businesses with low profit, administrative costs may outweigh the expected tax benefit.

A Cyprus company can be beneficial for a business that has international revenue, works with partners in the EU, requires a holding structure, or plans legal tax planning. It is less appropriate for local small business without foreign economic activity if maintenance costs exceed savings.

Feasibility should be assessed through a financial model. It is important to consider profit, client countries, payment currencies, banks, owners, future dividends, beneficiary tax residency, and reporting requirements.

For companies with profits that do not cover audit, administration, and support costs, Cyprus may be a premature choice. In such cases, it is advisable first to assess turnover, margin, and owner jurisdiction.

A Cyprus structure is not always justified for entrepreneurs operating only in their domestic market or unwilling to maintain full accounting. It can also be unfavorable if the owner simply wants “low tax” without a real corporate model.

Problems often arise when a company is established without analyzing clients, banks, VAT, CFC rules, and future dividends. As a result, the business gains not optimization, but an additional level of administration.

For such cases, it is better to compare Cyprus with a local company, sole proprietor model, another European jurisdiction, or a structure with simpler administration.

IT companies often consider Cyprus due to the combination of corporate tax rate, IP Box, access to European clients, and the ability to work with banks and payment systems. However, the tax model depends on whether the company sells development services, licenses a product, receives royalties, operates as SaaS, or owns IP.

For service IT business, the key is correct pricing, client contracts, developer arrangement, and defining the place of service delivery. For product business, IP rights, IP documentation, R&D expenses, and licensing structure are additionally important.

Cyprus can be convenient for IT but only with properly formalized intellectual property rights. If developers, management, and clients are actually located in another country, a separate risk analysis is required.

Trading companies use Cyprus for contracts with suppliers, buyers, distributors, and logistics partners. The tax burden depends on margin, VAT, customs procedures, the place of goods storage, and delivery terms.

If the goods do not physically enter Cyprus, it does not automatically mean no tax consequences. It is necessary to analyze the route of the goods, ownership rights, incoterms, place of delivery, country of import, and documents.

A trading structure in Cyprus requires clear documentation. Banks and tax advisors check not only invoices but also the reality of deliveries, logistics, counterparties, and the commercial role of the Cypriot company.

Cyprus is often used as a holding jurisdiction for owning shares in foreign companies. Such a model may be appropriate for business groups, investors, M&A deals, ownership of subsidiaries, and centralization of dividends.

The tax effect depends on participation in subsidiaries, source of dividends, double tax treaties, rules of the subsidiary’s country, and beneficiary status. The mere fact of a Cypriot company does not guarantee tax savings.

The holding model requires special attention to substance. The director, corporate decisions, bank account, minutes, contracts, and strategic functions must confirm the real role of the Cypriot company.

Substance is the economic presence of a company in the jurisdiction. For Cyprus, it has practical significance due to banks, tax authorities, double taxation treaty rules, and checks from other countries.

Substance does not always mean a large office and dozens of employees. It concerns aligning the scale of presence with the actual activity of the company.

If necessary, the structure may include a nominee service, but its use must be legally correct, properly documented, and should not substitute actual management where factual presence is required.

Order nominal service for your business on this page.

Before launching a business, it is important to determine which is more advantageous – to create a new company or buy a ready-made firm. Tax-wise, both options can work equally well, but they differ in company history, banking checks, risks from previous activities, and speed of start-up.

A ready-made company requires due diligence. It is necessary to check whether it had transactions, debts, tax liabilities, VAT registration, bank accounts, contracts, or outstanding reports.

Before choosing a format, a consultation on company registration is required, as the speed of launch should not outweigh tax cleanliness, banking acceptability, and future reporting requirements.

Tax planning in Cyprus should be calculated together with administrative expenses. The company has costs for registry, secretary, office address, accounting, audit, tax declaration, banking compliance, and legal support.

For small businesses, it is important to compare the expected savings with the real cost of the structure. If the company earns little or has no international need, the expenses may be disproportionate.

The optimal structure is not necessarily the cheapest. It must correspond to turnover, risks, markets, banking requirements, and the owner’s plans regarding dividends or reinvestment.

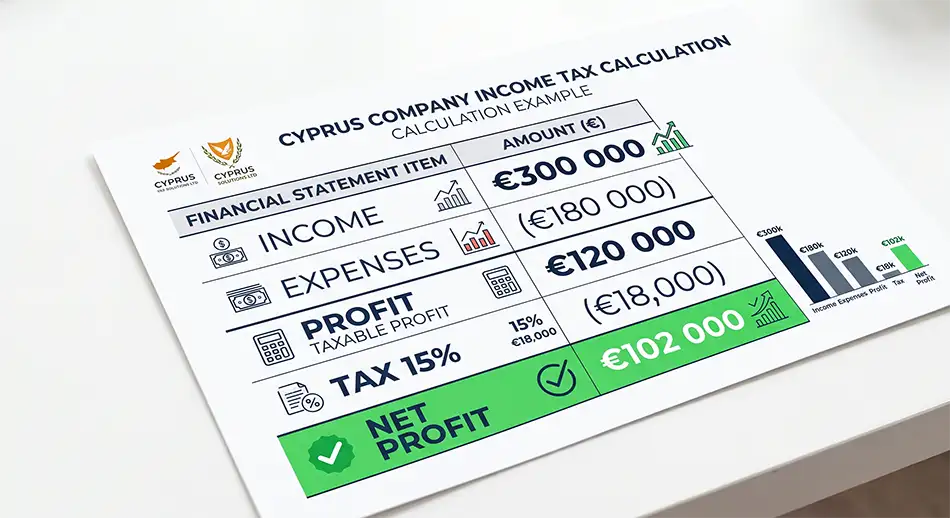

For a basic understanding, one can take a company with income of €300,000, expenses of €180,000, and profit before tax of €120,000. If no special benefits apply, the corporate tax at a rate of 15% will amount to €18,000.

This calculation is simplified, as the real base may change due to unrecognized expenses, depreciation, IP Box, Notional Interest Deduction, losses from previous years, transfer adjustments, or features of specific income.

This example shows the principle but does not replace the tax model. For companies with IP, financing, international trade, or group operations, the effective rate may differ.

Most problems with Cyprus companies arise not because of the tax rate but due to improper structure preparation. Mistakes often accumulate over the year and are revealed during audit, banking checks, or tax inquiries.

Particularly risky are situations when the company is used for payments without contracts, without service confirmation, or without a clear connection between income and expenses.

Correcting such mistakes is usually more expensive than setting up the structure correctly from the beginning. The best model is one where tax, corporate, and banking requirements are considered before the first payments.

Before creating or buying a company, a preliminary analysis should be conducted. It helps to understand whether Cyprus will provide tax, operational, or reputational benefits specifically for the given business.

The evaluation should include not only the tax rate but the entire money chain – from the client to the company, from the company to the owner, and from the owner to their personal declaration.

Only after such analysis can the real efficiency of a Cyprus company be assessed. In a professional structure, tax savings should be a consequence of a legitimate business model, not the sole reason for setting up a company.

From January 1, 2026, the standard corporate tax rate is 15%. The tax applies to the company’s taxable profit, not the entire turnover.

Yes, Cypriot companies usually must prepare financial statements and undergo an audit. The audit serves as the basis for the tax return, annual return, and corporate compliance.

Yes, VAT applies to goods, services, imports, and certain transactions with the EU. The standard rate is 19%, but there are reduced and zero rates.

VAT registration is required if taxable turnover exceeds €15,600 within 12 months or is expected to exceed this threshold within 30 days. Additional grounds for registration may apply for EU transactions.

Yes, if the IT company has international clients, a product model, IP assets, SaaS revenues, or needs a European structure. At the same time, it’s necessary to properly arrange rights to the code, contracts with developers, VAT, and tax residency.

It is possible if income is related to qualified intellectual property and the regime conditions are met. Simple provision of IT services without a distinct IP asset usually does not automatically grant IP Box rights.

Cyprus may be appropriate for holding structures if there are foreign subsidiaries, dividends, investments, or future business sale deals. Analysis of double taxation treaties and the beneficiary country’s rules is required.

Actual management from another country can create the risk of tax residency outside Cyprus. For an international structure, management, documents, director decisions, and substance need to be properly arranged.

Cyprus might be unprofitable for small businesses with low income if administration, audit, and support costs exceed the tax benefit. Feasibility should be calculated through a financial model.

The company needs contracts, invoices, bank statements, acts, expense confirmations, payroll documents if staff are present, VAT documents, directors’ minutes, and documents regarding related-party transactions.