How the Polish Tax System Works Business taxation in Poland depends on the legal-organizational form, residency, type of activity, turnover, and profit distribution method. A limited liability ...

17Jul

Switzerland is traditionally regarded as one of Europe’s most stable jurisdictions for doing business, but its tax model requires precise analysis even before a company is incorporated. Unlike countries with a more centralized system, Swiss taxation is built on tax federalism, where not only federal rules matter, but also the rules of the specific canton and municipality.

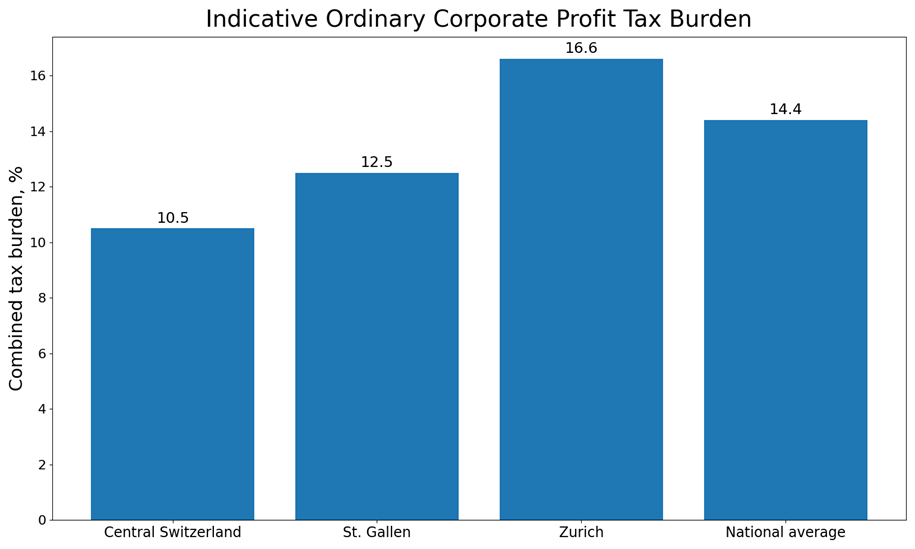

For an investor, the owner of an operating company, a holding structure, a trading business or a service business, this means one thing – the actual tax burden in Switzerland must always be calculated individually. Formally, the federal corporate income tax rate is uniform, but the effective combined rate depends on the place of incorporation, capital structure, nature of income, presence of personnel, international payments and the cantonal tax planning tools available.

In this article, we examine how the Swiss tax system works for business, which taxes companies pay, when VAT obligations arise, how incentives are applied after the TRAF reform, and how to properly organize tax reporting and compliance.

You can order professional advice from an international financial lawyer regarding taxes in Switzerland on this page. If you are interested in registering a company in Switzerland, you will be helped here. You can also order and buy a ready-made company in Switzerland.

Before moving into a detailed analysis, it is useful to see the basic benchmarks that most business projects in Switzerland rely on. These indicators do not replace an individual calculation, but they help quickly understand the architecture of the system.

| Indicator | Base value |

| Federal corporate income tax | 8.5 percent. |

| Average ordinary level nationwide | 14.4 percent. |

| VAT registration threshold | CHF 100,000. |

| Standard VAT rate | 8.1 percent. |

| Reduced VAT rate | 2.6 percent. |

| Special VAT rate | 3.8 percent. |

| Annual VAT reporting upon request | up to CHF 5,005,000 turnover. |

| Pillar Two | for groups with global turnover from EUR 750 million. |

Table 1. Basic tax parameters for business in Switzerland. Sources – EFD, ESTV, KMU Portal.

These benchmarks are a starting point for an initial review. Final tax modeling should always take into account the canton, municipality, type of income, presence of employees and international payments.

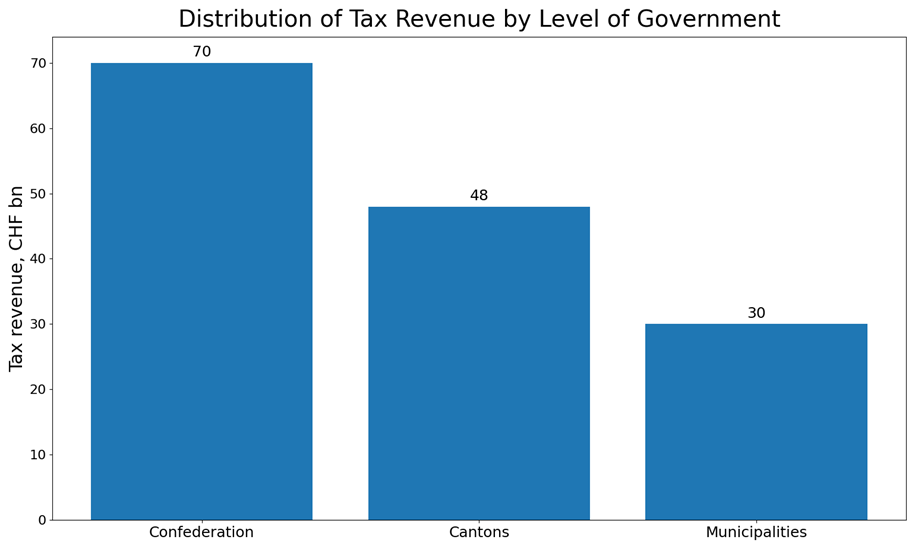

The Swiss tax system is based on the principle of federalism. This means that tax powers are divided between the Confederation, the cantons and the municipalities, so a business must assess not only national rules, but also local tax conditions.

It is this multi-level structure that explains why two companies with the same business model may have different tax outcomes in different cantons. To understand the system correctly, it is worth starting with the following core elements.

For businesses, it is important from the outset to understand which taxes are federal and uniform across the country, and which change significantly depending on the place of business. This distinction helps build the tax map of the future company correctly.

Thus, Swiss tax federalism is not merely a theoretical feature of the state structure. For business, it is a practical factor that affects costs, the group structure, the location of personnel and the overall profitability of a project.

The tax status of a company in Switzerland is determined not only by the fact of legal incorporation. The place of effective management, the nature of the activity and the presence of an economic footprint in Switzerland are also highly important.

For foreign investors, this is especially important, because a tax nexus with Switzerland may arise even without creating a separate Swiss legal entity. In basic terms, the following situations should be distinguished.

Properly classifying the structure at the project launch stage helps avoid disputes over residence, incorrect VAT registration and double taxation.

Податкове навантаження швейцарської компанії складається з кількох блоків. Частина податків The tax burden of a Swiss company consists of several blocks. Some taxes depend on profit, others on turnover, capital, cross-border payments or corporate actions such as an increase in share capital.

To see the full picture, taxes should be viewed not as a single payment but as a system of interrelated obligations. In practice, businesses most often deal with the following tax categories.

That is why a tax review before entering the Swiss market usually includes not only a calculation of the corporate income tax rate, but also an assessment of the entire system of fiscal obligations.

For most entrepreneurs, the central issue is the taxation of profits. At the federal level, Switzerland applies a rate of 8.5 percent to the net profit of companies, but this is only one part of the actual tax burden.

Once cantonal and municipal taxation is added, the combined result changes significantly. In practice, a business should take the following principles into account.

As a rule, expenses that may be taken into account for tax purposes include economically justified business expenses. However, the tax authorities carefully examine the business purpose of expenses and the reality of transactions.

The greatest risks for business arise when payments to the owner or related parties in fact disguise a distribution of profits.

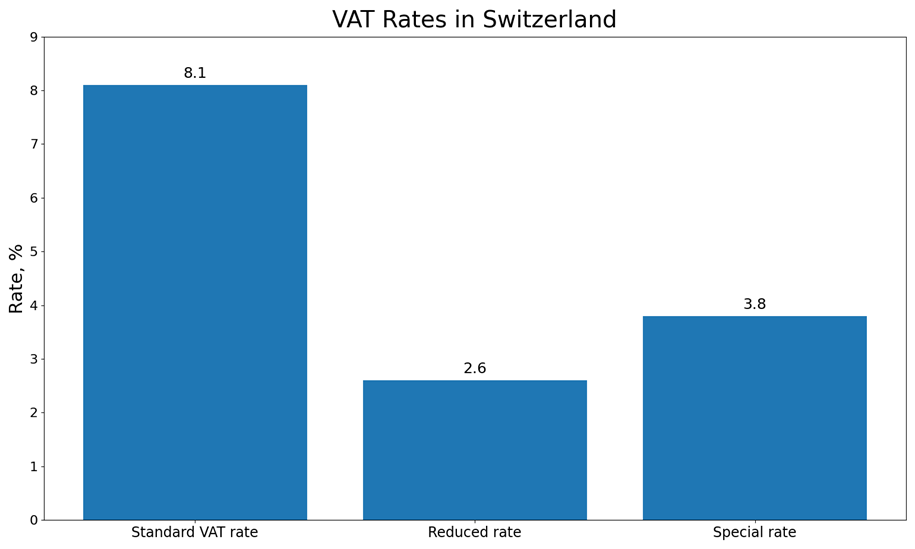

VAT in Switzerland is administered at the federal level and is one of the most important taxes for operating businesses. It applies not only to Swiss companies but also to foreign suppliers carrying out taxable transactions connected with Switzerland.

The basic threshold for mandatory VAT registration is CHF 100,000 of turnover from relevant transactions. After registration, a business must correctly determine the rate, place of supply, entitlement to input tax deduction and reporting deadlines.

For many companies, not only registration but also the reporting format is important. Since 1 January 2025, annual VAT reporting upon request has been available to businesses with annual turnover of up to CHF 5,005,000, which reduces the administrative burden.

Below are the basic VAT rates used in the Swiss system.

For foreign companies, the rules on supplies of services, goods, low-value consignments, imports and the use of electronic platforms should be analyzed separately.

Capital tax is not levied at the federal level in Switzerland, but at the cantonal and municipal levels it remains important for holdings, financial structures and companies with significant capitalization.

The standard Swiss withholding tax rate on investment income is 35 percent. The final economic result depends on whether a refund is available, the terms of the applicable international treaty and the correct corporate structure.

After the TRAF reform, Switzerland abandoned the old preferential regimes for status companies and moved to instruments compatible with international standards. For business, this means that tax planning has not disappeared – it has changed its form.

For new projects, start-ups and investment structures, not only tax losses, international treaties and OECD rules matter, but also employment compliance. If a company has employees in Switzerland, social contributions, payroll and insurance must be addressed simultaneously with the corporate and VAT structure.

The supplementary tax for large groups has applied since 1 January 2024, and the income inclusion rule – since 1 January 2025. These rules apply to groups with global annual turnover of EUR 750 million or more.

An employer in Switzerland must plan not only for corporate taxation, but also for mandatory payments associated with hiring employees. For a business with local personnel, this block is a mandatory part of the financial model.

The Swiss tax system is considered predictable, but this does not mean it can be administered in a simplified way. A business must ensure timely registration, correct classification of income, accounting, storage of primary documents and the filing of reports within the proper deadlines.

To make entry into the Swiss market tax-safe, it is worth acting consistently. Each of these steps affects the next one, so skipping even one stage often leads to structural errors.

Taxes for business in Switzerland are a multi-level system combining federal rules, cantonal autonomy and municipal features. That is why effective tax planning here begins not with a search for the «lowest rate», but with building the right business model.

For a company planning to enter the Swiss market, it is critically important to assess corporate income tax, VAT, capital tax, withholding tax, stamp duties, personnel-related charges, the availability of incentives and the international dimension of the structure. If this is done at the planning stage, Switzerland can become not only a prestigious jurisdiction, but also a tax-efficient one for the stable development of business.й аспект структури. Якщо це зробити на етапі планування, Швейцарія може стати не лише престижною, а й податково ефективною юрисдикцією для стабільного розвитку бізнесу.